Photo Credit: Mike Mozart

Key Takeaways

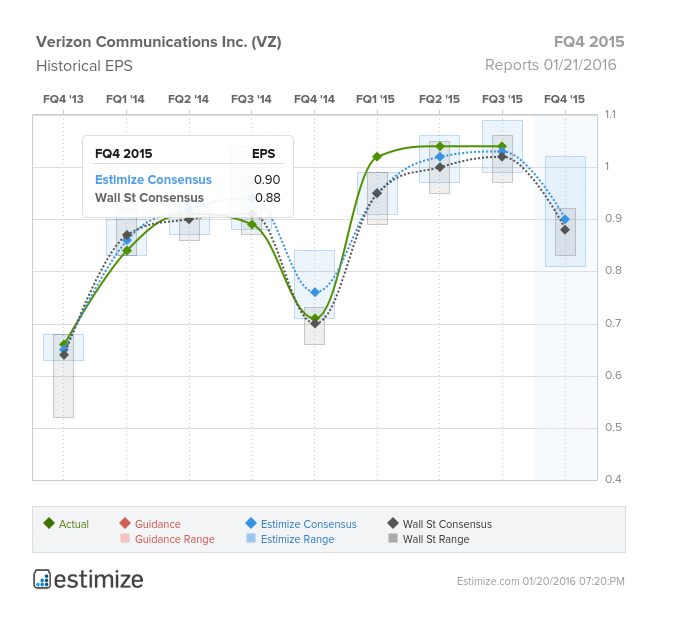

Once the dominant player in telecom, Verizon (VZ

Over each quarter of 2015, Verizon beat estimates with continual growth of its subscriber base. A major component of Verizon's revenue is consistently drawn from the number of subscribers to its service. At the moment, wireless services accounts for almost 70% of Verizon's revenue with the remainder coming from various different sources. Despite stiff competition, Verizon enjoys a strong foothold in the wireless market and expects to grow as they continually roll out new products and services. The telecom company routinely introduces new 4G products and has now experimented with 5G technology. Superfast connections not only leverage one company over the other, but is essential to the exponential growth of Internet connected devices. Verizon has also churned out new products to increase its exposure as a leading content provider. In late 2015, Verizon introduced its mobile video streaming service , Go90 to target users on the go. Moreover, the telecom company operates a fiber optic network, Verizon Fios, and acquired AOL in mid 2015, further driving revenue growth. Verizon faces a number of short term threats, including a saturated wireless market, intensifying competition, heavy capital spending and regulatory risks. Regardless, Verizon's upside should outweigh the downsides coming into their Q4 2015 earnings this Thursday.